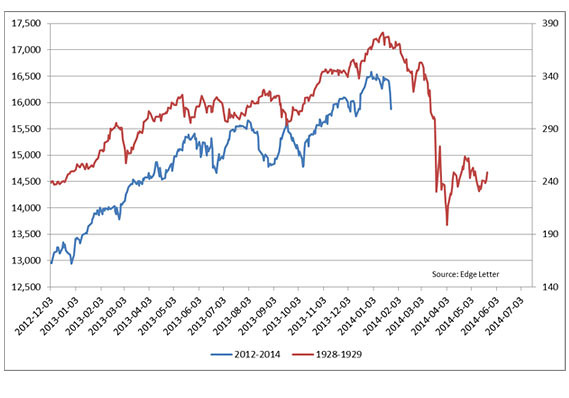

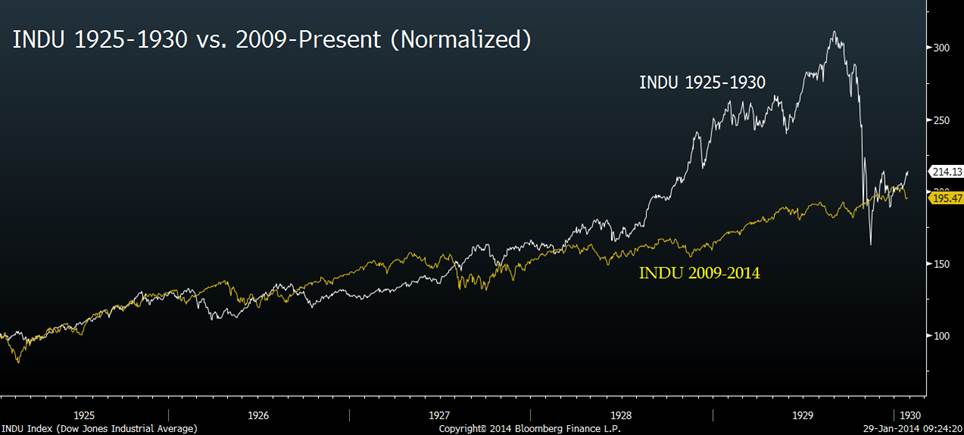

against all odds

Seite 59 von 117 Neuester Beitrag: 08.04.20 16:14 | ||||

| Eröffnet am: | 22.03.13 19:18 | von: Fillorkill | Anzahl Beiträge: | 3.904 |

| Neuester Beitrag: | 08.04.20 16:14 | von: Fillorkill | Leser gesamt: | 342.801 |

| Forum: | Börse | Leser heute: | 67 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 56 | 57 | 58 | | 60 | 61 | 62 | ... 117 > | ||||

Optionen

Optionen

Optionen

Optionen

Die Zinserhöhung in der Türkei erinnert mich an die 70er, als Volker mit seiner Zinserhöhung der Inflation erst mal ein Ende gesetzt hat.

Optionen

Angehängte Grafik:

geist.jpg (verkleinert auf 89%)

geist.jpg (verkleinert auf 89%)

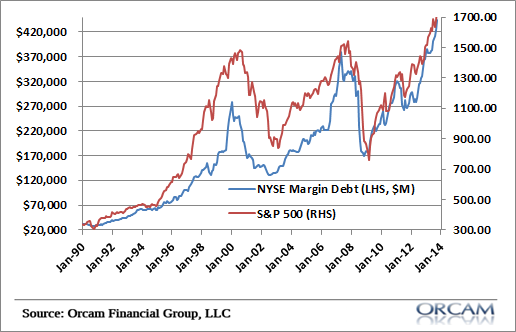

Türkei: Das Problem ist wie immer die exzessive private Verschuldung. Schwundwährung, sparender Staat und Mondzinsen werden die Gesamtersparnis auf 0 sinken lassen, ein dramatischer Einbruch im GDP wird also angezeigt. Auf die importierte Inflation wird die NB sicher nur marginalen Einfluss nehmen können...

Optionen

The demand and issuance of credit can occur for many different economic transactions and purposes. This can involve productive and unproductive uses. A simple example of productive uses would be a corporation that maintains a line of credit with a bank in order to pay its expenses such as salaries, R&D or other investments. As we like to say with MR, "investment is the backbone of private saving". This is the essential idea behind understanding our central equation S=I+(S-I). But there are also unproductive uses of credit. For instance, when loans are made to meet the growing demands of speculative real estate purchases you get environments like 2003-2007 where asset prices simply inflate due to the extension of credit for unproductive uses. This is the essence behind the idea of a disaggregation of credit. It is essential to understand that all credit is not created equal. Money can be abused for the purposes of profit. This is not remotely surprising in a capitalist monetary system like the USA. But this is not an excuse for not understanding this concept.

While most of the economics profession is busy building government centric models that figure out various ways to blame the government (or give it credit) it"s equally important to understand how the private sector itself can be the cause of this economic disequilibrium. Understanding the design of the modern monetary system and the concept of disaggregation of credit is central to this understanding...'

http://pragcap.com/the-disaggregation-of-credit

disaggregation of crecit:

Optionen

Angehängte Grafik:

md2.png (verkleinert auf 98%)

md2.png (verkleinert auf 98%)

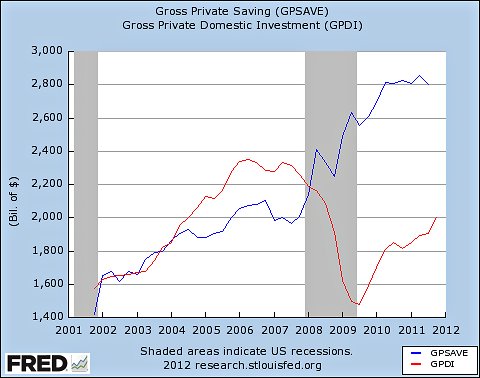

Private sector saving (S) = investment (I) plus private sector net financial asset accumulation (S-I)

The blue line = S

The red line = I

The gap between the blue line and the red line = (S – I)

Optionen

Angehängte Grafik:

si.jpg

si.jpg

The basic idea of explaining equality between saving and investment is that it is brought about by changes in income and not through the mechanism of interest rate.

According to the functional equality version when people save more than what the investors think it worthwhile to invest, the demand for consumer and producer goods falls down. When the goods produced are not profitably sold, the entrepreneurs curtail production of goods and the national income falls. If investment is more than saving, the national income rises. The process of changes is income, saving and investment continues till saving and investment are in equilibrium (was jedoch nie der Fall ist)

http://economicsconcepts.com/...identity_of_saving_and_investment.htm

Optionen

Anyhow, it would be my hope that this starts to reframe the discussion a little bit. Economics is too important to be left entirely to biased theorists who refuse to try to better understand reality. But I doubt anyone will seriously consider changing their models much because that would also involve a lot of mea culpas. And since we’re totally irrational animals, we’d prefer not to deal with mea culpas because then everyone might perceive us as being weak even though the mea culpa will actually improve our thought processes. Oh well....'

http://noahpinionblog.blogspot.de/2014/01/...rences-are-unstable.html

Optionen

Optionen

Angehängte Grafik:

image001.jpg (verkleinert auf 52%)

image001.jpg (verkleinert auf 52%)

Die EMA's machen teilweise tiefere Tiefs und tiefere Hochs. Das nennt man Verkaufsdruck.

Bei einigen Schwergewichten wie Beiersdorf, Münchner Rück oder Siemens gibt es ebenfalls Anzeichen von Topbildungen. Aber auch diese sollten kurzfristig oversold sein und etwas zurück kommen. Sehen wir in Kürze keinen bullischer Trigger, werde ich wohl den nächsten Spike shorten.

Bin noch long Stoxx 50 und warte auf den Spike.

Kann deine vielen Beiträge gar nicht würdigen, da ich so gut wie keine Zeit und vor allem keine Energie habe. Der Job frisst mich gerade auf.

Optionen

Optionen

Angehängte Grafik:

unbalanced_small.jpg

unbalanced_small.jpg

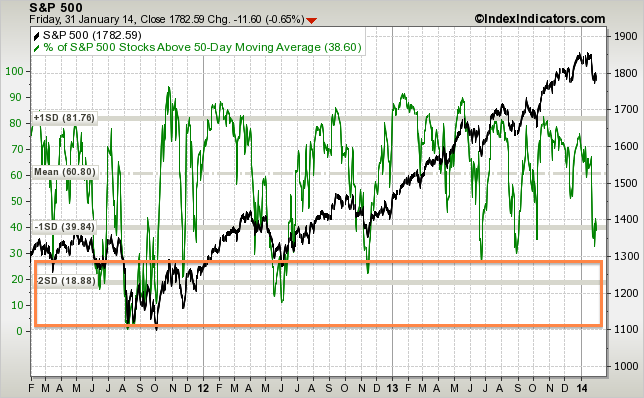

Angehängte Grafik:

sp500-vs-sp500-stocks-above-50d-sma-params-....png (verkleinert auf 79%)

sp500-vs-sp500-stocks-above-50d-sma-params-....png (verkleinert auf 79%)