Ariad Pharma on the Top

Seite 155 von 373 Neuester Beitrag: 26.09.16 18:45 | ||||

| Eröffnet am: | 17.01.14 10:56 | von: Masterbroker. | Anzahl Beiträge: | 10.311 |

| Neuester Beitrag: | 26.09.16 18:45 | von: Masterbroker. | Leser gesamt: | 1.460.062 |

| Forum: | Börse | Leser heute: | 445 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 153 | 154 | | 156 | 157 | ... 373 > | ||||

Sah ja auch alles ne ganze weile voll geil aus aber 3 Tage Siesta in Amiland hält da keiner

durch.

Mit 17 Mill. Shares ging es Hoch, mit weiteren 8 Mil. wurden immer wieder die 8.88 verteidigt und am schluß haben schlappe 3 Mio. gereicht um einigen das Wochenende zu versauen.

Schön ist aber das die heute Grün war und somit ein Kaufpaket

Optionen

| Boardmail an "MasterbrokerUSA" |

Wertpapier: ARIAD Pharmaceuticals, |

Da ist am Ende jetzt fast so ein hässlicher " Inverted Hammer" bei rausgekommen.

Angehängte Grafik:

ariad_inverted_h.png (verkleinert auf 56%)

ariad_inverted_h.png (verkleinert auf 56%)

Optionen

| Boardmail an "MasterbrokerUSA" |

Wertpapier: ARIAD Pharmaceuticals, |

Optionen

| Boardmail an "MasterbrokerUSA" |

Wertpapier: ARIAD Pharmaceuticals, |

Wenn ihr keinen Mut zum Verkaufen habt dann solltet ihr wenigstens die ......

LG

Thom

Stifel:Iclusig Usage Expected to Increase Over Next 12 Months, Including in 2nd-Line CML Patients Without T315i

Angehängte Grafik:

stif3.gif (verkleinert auf 51%)

stif3.gif (verkleinert auf 51%)

Next Steps for Clinical Strategy

Credit Suisse / Jan 15, 2014

[Posted for background information. Even though brokerage report is only

two weeks old it seems ancient given all the recent developments. - A]

Iclusig will be made available again in the US later this month following the

FDA's approval of the new label and the risk evaluation and mitigation strategy

(REMS). ARIA has plans to clarify the dose/safety relationship of the drug and

to push into new indications. We remain cautious pending new launch metrics,

and expect ARIA will need to raise additional capital in 2014.

¦ EPIC data to be presented at 2014 ASCO meeting. ARIA expects to

present available clinical data for the Phase III EPIC study in front-line CML

patients at the upcoming ASCO meeting (May 30-June 3). The presentation

will likely focus on the safety analyses and will include data from

approximately 300 patients. This is the first safety analysis with an active

comparator (Gleevec), which could potentially have commercial implications.

¦ ARIA still has aspirations for the front line CML indication. Management

indicated that it is still interested in pursuing the front-line setting. This will be

gated by the upcoming dose exploration study expected to recommend an

optimal dose for front line patients. Even if ARIA started a new front line trial

in 2015, it will likely take two to three years to complete, by our estimates.

¦ GIST indication likely to become a key focus. ARIA reported the first

anecdotal data for Iclusig in GIST. This study was nearly fully enrolled once

the partial clinical hold was put in place, and ARIA expects to present initial

data from the GIST trial at ASCO. Recall that approximately $1.4B of the

2012 Gleevec annual sales were largely attributable to its GIST indication,

suggesting this is a large marketing opportunity.

¦ ARIA provides outline of registrational AP26113 trial

ARIA will initiate a pivotal trial of AP26113 in ALK+ NSCLC patients that are Xalkori

resistant in Q1:14. The trial will enroll approximately 220 patients, and will include patients

with brain metastases. All patients will be dosed with 90mg QD for one week, then patients

will be randomized 1:1 to receive either a 90mg or 180mg dose. The primary endpoint is

ORR, and CNS response will also be measured. Twenty patients in the Phase I

exploratory study have been dosed at 90mg for one week and then 180mg thereafter, and

none of these patients reported developed the pulmonary syndrome observed in earlier

dose cohorts.

¦ Still strong interest in investigator sponsored trials of Iclusig

ARIA indicated that nine ISTs are expected to start in 2014. The diseases to be examined

include: (1) Elderly Ph+ ALL, (2) Blast Phase CML, (3) AML, (4) endometrial cancer, (5)

FGFR mutant cancers or other cancers with mutations in other ponatinib targets, and (6)

bile duct carcinoma. We believe this is a positive sign for the Iclusig franchise, as it

suggests that physicians are not overly concerned about the side effect profile and view

the risk/benefit reward favorably for certain cancer types.

¦ ARIA increased Iclusig price 8.0%

ARIA increased the price of Iclusig by 8.0% late last December. Other companies

marketing a TKI also took increases in the past several months. Iclusig is still priced at

premium to other TKIs.

von http://www.siliconinvestor.com

Ariad is re-launching with a slimmed down field force roughly half the size of the previous sales force of 65. The company indicated there were a total of 370 requests for drug under the IND process of which they shipped drug to 305. As of January 16th, the company began converting those patients to commercial drug. Importantly, many treated patients are still finishing doses from the IND process, suggesting to us that the true sales ramp for the re-launch begins this month. Ariad also indicated that for competitive reasons they are not reporting sales to IMS and are only using

one specialty pharmacy compared to nearly 10 in 2013.

Our analysis of IMS weekly script data shows that under 25% of Iclusig patients switched to either Bosulif, Tasigna, or other treatments following Iclusig suspension. We see this as indicative of the lack of consensus options to replace Iclusig and view this positively for the positioning of Iclusig as a viable late-line therapy. As patients finish their January doses of CML drug, we expect to see a decrease in scripts as patients switch back to Iclusig and will look to this metric to gauge re-adoption of Iclusig.

We believe Iclusig has the potential to slowly gain share in earlier lines of therapy for CML, and approach $500M in U.S. sales by 2018. For chronic phase patients, management suggested therapy duration of 3-4 years is reasonable, which is higher than our average estimate of 18 months, suggesting potential upside to our estimates. Given 1300 U.S. patients that fail two or more TKIs each year (including 315i patients) at a net annual price of ~$113k and 3.5 year duration of therapy, we arrive at greater than $500M annual US market opportunity with significant upside potential based on penetration into the 2600 annual incidence of 2nd line patients. We note that ~30% of patients on Gleevec fail after three months of therapy, so we believe that there is upside potential to the size of the second line population.

Though Iclusig's approval is for third-line and T315i mutants, we note that approximately 25% of the patients on commercial drug in 2013 were second-line patients, and that approximately 20% of the patients on IND access were second line patients. We view this as supporting our 31% estimate of 2014 second line patients. This segment of Iclusig usage is important because duration of therapy increases substantially in earlier lines of therapy and could exceed 10 years. Management believes that they have room to be more aggressive on increasing price, but that they are reluctant to pursue greater increases in order to preserve the opportunity in the second line, pending further data and a label expansion.

We reduce our 4Q13 Iclusig ex-US revenue estimate to $7.3M from $11.3M to recognize that sales from certain countries will require deferred revenue recognition. This is due to the ongoing price negotiations, for example

in France. Management indicated France and Italy should contribute to EU sales by 2H14.

The low dose Iclusig trial is on track to start in 2H14 with data by year-end 2015. The intention of the trial is to determine if Iclusig could maintain its efficacy at a lower dose while improving tolerability. If so, it could facilitate usage in earlier lines of therapy. We see the analysis of the PACE trial presented at ASH that showed a 40% decrease in CV events for each 15mg decrease in dose as a framework from which to work from for this trial. We note that in that trial, 96% of complete cytogenic response patients who had their dose reduced maintained the CCR through dose reduction.

GIST remains another area of potential upside for Iclusig. Management expects FDA to soon lift the clinical hold on the current study in GIST. Given the trial has already enrolled 43 of 50 targeting patients and most continue to

receive drug, the trial should not take long to complete, and will now incorporate dose reductions. Investigators showed promising data from 1 patient in January that showed shrinkage of progressive lesions in a patient who had progressed on 4 previous therapies.

Source: Stifel/Sendek, February 5, 2014

auch von http://www.siliconinvestor.com

Er sieht wohl eine Unterstützung kurz unter 8,50 $ die es zu halten gibt.

Na da bin ich mal gespannt

Nur meine Meinung, natürlich auch Verluste möglich

hoffentlich auch in die richtige Richtung. Könnte durchaus sein das wir am 25.02. eine böse Überraschung erleben. Die Zahlen werden echt mies sein. Bei Oramed hab ich es erlebt das der Kurs von nem Investor schön in die Höhe getrieben wurde und dann waren die aufeinmal weg.

Ich denke das es hier ähnlich werden könnte und die grossen vorher aussteigen. Was denkt ihr?

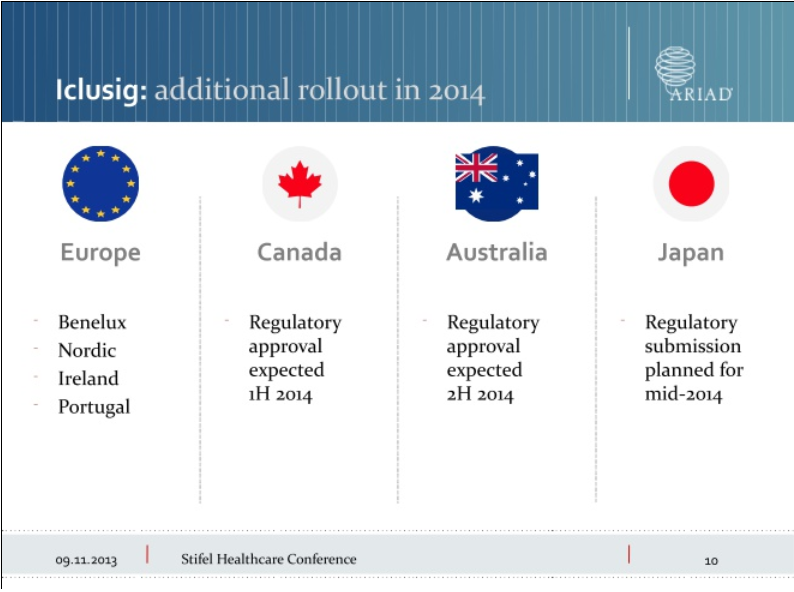

Jederzeit könnte ne neue Zulassung kommen, Schweiz liegt ja sehr gut im Rennen. Oder sogar erst Kanada oder Japan? Ich bin entspannt, Capret- Ariad Langzeitinvestor aus Überzeugung, für alles andere hab ich nen SL in sicheren Abstand :b

Mal gespannt auf das ASCO meeting 30.05. - 03.06. Fortschritt in der pipe? Siehe #3859

Angehängte Grafik:

rollout_2014.png (verkleinert auf 64%)

rollout_2014.png (verkleinert auf 64%)

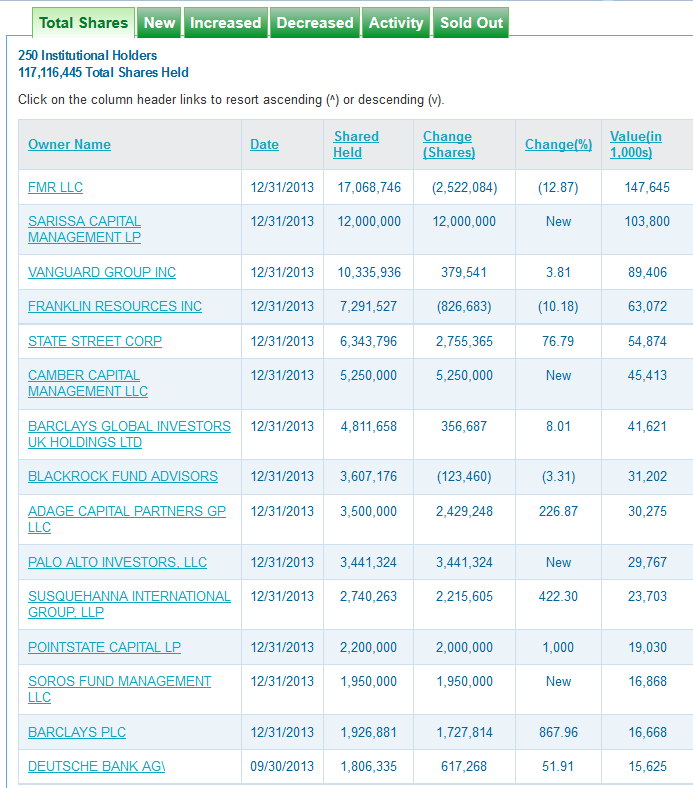

Vier Mal im Jahr läuft Börsen-Gourmets das Wasser im Munde zusammen. Sie erfahren, was die Großen an der Wall Street in ihre Depots legen. Ab einer Portfolio-Größe von 100 Millionen Dollar besteht Meldepflicht für alle Investoren.

http://www.n-tv.de/wirtschaft/...-Warren-Buffett-article12282366.html

---> Das gilt natürlich auch für die Ariad Zukäufe/Verkäufe, und da hat sich einiges geändert,

wobei der Institutional Ownership nur um 2% auf insgesamt 63% gefallen ist.

Angehängte Grafik:

holdings.png (verkleinert auf 73%)

holdings.png (verkleinert auf 73%)

Carpet, wie schätzt du das Szenario ein?

Optionen

| Boardmail an "Lobster2014" |

Wertpapier: ARIAD Pharmaceuticals, |

Optionen

| Boardmail an "Lobster2014" |

Wertpapier: ARIAD Pharmaceuticals, |

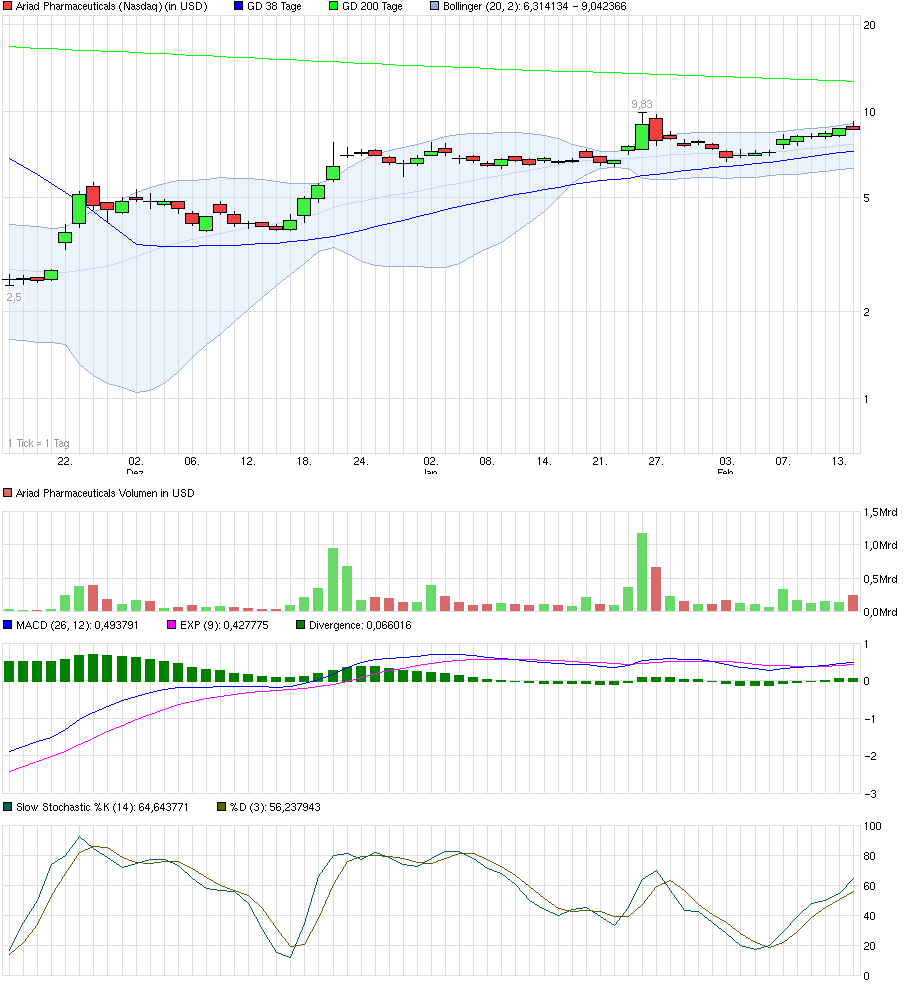

Vorallem ist es sehr ungewiss wie die nächste Woche verläuft. Wie sich der Kurs am Freitag entwickelt hat war sehr unschön. Befinden wir uns bis zu den Zahlen in einer abwartenden Seitwärtsbewegung, oder kommen die Freitagskäufer wieder zurück und es geht wieder hoch? Falls es nach Norden durchs BB geht evtl. sogar deutlich. Meinerseits hofft auf positive news in den Nächsten 48h, dann schaffe wir das auch :)

Haben jedenfalls noch viel Luft nach unten im Trendkanal, für mich auch sehr beruhigend.

Angehängte Grafik:

aria_day.png (verkleinert auf 31%)

aria_day.png (verkleinert auf 31%)

Optionen

| Boardmail an "MasterbrokerUSA" |

Wertpapier: ARIAD Pharmaceuticals, |