(BOI)denbildung abgeschlossen,

Seite 87 von 380 Neuester Beitrag: 25.04.21 00:01 | ||||

| Eröffnet am: | 16.12.12 10:31 | von: weltumradler | Anzahl Beiträge: | 10.487 |

| Neuester Beitrag: | 25.04.21 00:01 | von: Petraqssia | Leser gesamt: | 2.365.610 |

| Forum: | Hot-Stocks | Leser heute: | 223 | |

| Bewertet mit: | ||||

| Seite: < 1 | ... | 84 | 85 | 86 | | 88 | 89 | 90 | ... 380 > | ||||

Cameron

schönes we auch allen

Optionen

| Boardmail an "kowaltzki" |

Wertpapier: Bank of Ireland plc |

glaubst du denn, wenn du hier nahezu zum alleinunterhalter wirst mit deinen 30 postings pro tag wirds besser ....?!.......mein gott eh

Ich bin der Meinung, und andere bestimmt mit mir, das CAMERON bisher recht gute, sachliche Beiträge geleistet hat, die ich lieber lese, als Deine marktschreierischen Ausbrücke. Nix für ungut!

1 November 2013 | 14:50pm

StockMarketWire.com - Bank of Ireland's positive momentum in re-building its net interest margin has continued since the end of June and averaged over 190bps during the third quarter to 30 September.

The group says this reflects the on-going actions being taken by management to reduce the cost of money, reprice assets and restructure the balance sheet. The group says fees for the exceptional liabilities guarantee are reducing in line with expectations and other income is broadly in line with the first half of 2013.

- See more at: http://www.stockmarketwire.com/article/4698146/...thash.HBq6lIVh.dpuf

Optionen

| Boardmail an "bvb189" |

Wertpapier: Bank of Ireland plc |

The Governor and Company of the Bank of Ireland (The "Group")

Interim Management Statement

1 November 2013

Trading

The positive momentum in re-building the Group's net interest margin (NIM) has continued since 30 June 2013, with an average NIM in excess of 190bps achieved during the third quarter to 30 September 2013. This reflects the on-going actions being taken by management to reduce the cost of money to the Group, reprice assets and restructure the Group's balance sheet.

Fees for the Exceptional Liabilities Guarantee (ELG) are reducing in line with expectations.

Other income is broadly in line with the first half of 2013.

We have the capital and the liquidity available to support our growth objectives in Ireland and in our core overseas franchises. We are actively seeking new lending opportunities of the appropriate credit quality and at appropriate levels of return.

The Group remains focused on tight cost control while continuing to invest in its core franchises. Restructuring and redundancy programmes are on-going.

In October 2013, following conciliation under the auspices of the Labour Relations Commission, the Group agreed a shared solution with the Irish Bank Officials Association (IBOA) in respect of the largest Group sponsored defined benefit pension scheme, the Bank Staff Pensions Fund (BSPF). This shared solution involves changes to members' potential defined benefits which, on a fully implemented basis, would reduce the IAS 19 BSPF defined benefit pension deficit by approximately €400m and would be income positive for the Group. In return, the Bank would increase its support for the BSPF, above existing support arrangements, so as to broadly match the deficit reduction arising from proposed changes to potential defined benefits. The IBOA has recommended this solution to its members and an IBOA members' ballot will take place before the end of November 2013.

Asset Quality

The macroeconomic environments in Ireland and the UK, the main markets in which we do business with our customers, have remained broadly stable to slightly improved from the first half of the year and our loan portfolios are continuing to perform in line with our expectations. The Group is continuing to meet all targets for the provision of commercially appropriate restructuring arrangements to cooperating customers who are having difficulty in meeting contractual repayments. Total arrears in our Irish mortgage loan books stabilised in the third quarter of 2013, with the level of early arrears declining.

Balance Sheet

The Group's net loan volumes at the end of September 2013 were marginally below the c.€87 billion reported at 30 June 2013 while customer deposits were marginally above the c.€72 billion reported at 30 June 2013, resulting in a loan to deposit ratio of below 120% (30 June 2013: 121%).

Usage of wholesale funding has decreased further since 30 June 2013 and the Group has continued to demonstrate its access to international capital markets, including the issuance in September 2013 of 7 year Asset Covered Securities (ACS), backed by Irish mortgage collateral.

The Group's capital ratios are broadly in line with the levels reported at 30 June 2013 and remain significantly above regulatory requirements.

Other

In relation to the 2009 Preference Shares, while noting yesterday's posting on the European Banking Authority website1, the Group continues to proactively formulate and assess a range of options in relation to the 2009 Preference Shares with our assessment of such options carefully taking into consideration our various stakeholders including the regulatory authorities.

The Central Bank of Ireland is currently conducting a Balance Sheet Assessment of the credit institutions covered under the ELG, including the Group. This exercise is a point in time capital adequacy assessment and is reviewing the risk classification, the level of impairment provisions and the level of risk weighted assets associated with selected loan portfolios of the relevant institutions. It is expected that this exercise will continue during this fourth quarter.

The Group notes the recent Irish budget and associated Finance Bill including the introduction of an annual banking levy in each of 2014, 2015 and 2016. The Group estimates the levy will give rise to a charge of c.€40m per annum for the Group. The Group also notes the proposals to abolish the tax provision which currently restricts (by 50% in any year) the use of Irish tax losses carried forward by banks which participated in NAMA, including the Group. This change would accelerate the Group's ability to utilise its tax losses carried forward and consequently the recovery of its Irish deferred tax asset would be expedited. Of the Group's total deferred tax asset of c.€1.7bn at 30 June 2013, c.€1.1bn related to Irish tax losses.

____________________________________

1 Response to Question ID 2013_11 - "State aid instruments issued prior to 1 January 2014 and initially subscribed by the Member State that comply with the provisions of Article 483 may be grandfathered fully in accordance with this Article during the period from 1 January 2014 to 31 December 2017.

The subsequent sale of those instruments to private investors does not alter the grandfathering arrangements applicable to those instruments which are still considered state aid instruments for the purposes of the Article 483 of CRR. They will be disqualified from regulatory own funds from 1 January 2018 unless they are fully eligible to either Common Equity Tier 1, Additional Tier 1 or Tier 2 in their own right."

Ends

For further information please contact:

Bank of Ireland

Andrew Keating Group Chief Financial Officer +353 (0)766 23 5141

Mark Spain Director of Group Investor Relations +353 (0)766 23 4850

Pat Farrell Head of Group Communications +353 (0)766 23 4770

Optionen

| Boardmail an "bvb189" |

Wertpapier: Bank of Ireland plc |

http://www.stockmarketwire.com/article/4698146/...tains-momentum.html

Cameron

hier gute Beiträge zu unserer BOI leistet.

Nicht nur das, er ist freundlich, hilfsbereit und niemals beleidigend.

Wenn dieses Forum unter Ihrem Niveau ist, steht es Ihnen

selbstverständlich frei dieses zu verlassen.

Ich werden Ihnen auf jeden Fall keine Träne nach weinen.

Font Size

26 Share

Bank of Ireland College Green 2...22/11/201Pic Collins Photos

DONAL O’DONOVAN – 01 NOVEMBER 2013

BANK of Ireland said a levy introduced as part of Budget 2014 will cost the bank €40m a year. But the bank said it is able, and willing, to lend.

ALSO IN THIS SECTION

Michael O'Leary plays down new 'nice guy' Ryanair image

Ulster Bank 'needs new business model'

Ulster Bank news is vote of confidence but let’s not open champagne yet

Interhyp Baufinanzierung

Den Traum vom Eigenheim erfüllen! Bester Baufinanzierer lt Euro 8/13

interhyp.de/baufinanzierung

0€ norisbank Girokonto

0€ Kontoführung, 0€ Kreditkarte, weltweit kostenlos Bargeld abheben.

www.norisbank.de/Kredit

Ads by Google

The new tax on banks aims to raise €150m a year in 20144, 2015 and 2016, and is being levied on all the main banks based on the size of their deposits.

Bank of Ireland’s estimate for the cost of the levy means it expects to be hit with more than a quarter of the total charged. It is contained in an interim management statement (IMS) issued today.

Bank of Ireland’s share price has increased at the fastest pace of any lender in Europe this year. In its IMS it said it is rebuilding profitability. The bank said its net interest margin, the difference between what it pays savers for deposits and charges borrowers for loans, is now in excess of 1.9pc.

It is good news for the bank, but a sign that both savers and borrowers face a tougher environment.

The recovery in margins does mean new lending is a more attractive prospect for the bank, now.

“We are actively seeking new lending opportunities of the appropriate credit quality and at appropriate levels of return,” the statement said.

Optionen

| Boardmail an "bvb189" |

Wertpapier: Bank of Ireland plc |

21 Jun - Limited Benefit Seen For Ireland From ESM Bank Decision

28 May - Bank of Ireland Plans Unsecured Bond Sale

13 Mar - Ireland Imposes Targets on Banks to Solve Home Loans Cr..

LONDON--Bank of Ireland PLC (IRE), one of a small handful of banks to survive the country's severe debt crisis, said Friday the Group remains focused on tight cost control while continuing to invest in its core franchises.

The bank said restructuring and redundancy programs are on-going, and fees for the exceptional liabilities guarantee are reducing in line with expectations.

"We have the capital and the liquidity available to support our growth objectives in Ireland and in our core overseas franchises, and we are actively seeking new lending opportunities of the appropriate credit quality and at appropriate levels of return", it added.

The Group is continuing to meet all targets for the provision of commercially appropriate restructuring arrangements to cooperating customers who are having difficulty in meeting contractual repayments.

The Group's net loan volumes at the end of September were marginally below the 87 billion euros ($118.9 billion) reported at June 30 while customer deposits were marginally above the EUR72 billion reported during the same period.

Capital ratios remain significantly above regulatory requirements.

Bank of Ireland is considered to be the healthiest among a small surviving group of Irish lenders, including Allied Irish Banks PLC (ALBK.DB) and Permanent TSB, that required huge amounts of Irish taxpayers' cash when the country's commercial-property market collapsed five years ago. But Ireland's banks continue to struggle with non-performing home and small business loans that may mean they will in time require more capital, some analysts say.

The Irish government has said it is very confident it will emerge from its bailout when the last of the EUR67.5 billion of emergency loans are disbursed by the European Union and International Monetary Fund at the end of this year.

--Eamon Quinn contributed to this article.

Write to Razak Musah Baba at razak.baba@wsj.com; Twitter: @Raztweet

Subscribe to WSJ: http://online.wsj.com?mod=djnwires

(END) Dow Jones Newswires

November 01, 2013 11:55 ET (15:55 GMT)

Copyright (c) 2013 Dow Jones & Company, Inc.

Optionen

| Boardmail an "bvb189" |

Wertpapier: Bank of Ireland plc |

Moderation

Zeitpunkt: 02.11.13 23:32

Aktion: Löschung des Beitrages

Kommentar: Beleidigung

Zeitpunkt: 02.11.13 23:32

Aktion: Löschung des Beitrages

Kommentar: Beleidigung

Optionen

| Boardmail an "bochum1848" |

Wertpapier: Bank of Ireland plc |

Allen anderen Usern wünsche ich einen schönen Abend trotz eines eher enttäuschenden BOI Tag. Bin seit ca. einem Monat (für mmm.aaa: mit mehr als 500 EUR) investiert und verfolge regelmäßig dieses Forum. Endlich mal ein aktives und informatives Forum, das von Posts wie von Cameron und Weltumradler lebt. Bitte weiter so.

Optionen

| Boardmail an "Elcanon" |

Wertpapier: Bank of Ireland plc |

Läuft doch...weiter so...

Optionen

| Boardmail an "Straßenfeger" |

Wertpapier: Bank of Ireland plc |

Optionen

| Boardmail an "Spaetschicht" |

Wertpapier: Bank of Ireland plc |

Mortgage arrears in Bank of Ireland’s loan book stabilised in the third quarter to the end of September, according to the bank, with the number of early-stage arrears falling.

The group, in which the State has a 15% shareholding, said it was meeting all of its targets in relation to providing restructuring arrangements for “cooperating customers” who are facing repayment difficulties.

It said the economies of Ireland and Britain had remained stable in the first of the year, with the bank’s loan portfolio performing in line with expectations.

Bank of Ireland also said its loan to deposit ratio fell below 120% in September as the restructuring of its balance sheet remained on-track.

The bank said its net loan volumes were marginally below the €87 billion figure reported at the end of June, while deposits were above €72 billion.

The bank, which the State has a 15% shareholding in, said its average net interest margin had grown to 190 basis points during the third quarter as a result of continuing attempts to reduce the cost of money to the bank.

It said its use of wholesale funding had fallen further in recent months, while the issuing of a seven year security in September showed it had access to international markets.

Optionen

| Boardmail an "bvb189" |

Wertpapier: Bank of Ireland plc |

Die BoI ist im laufe des Jahres um 126% schon gestiegen.Wir können dem Vorstand für seine gute Arbeit danken. Ich sehe für mich kein grund für den heutigen Verlauf in Panik zu verfallen. Gestern konnte man mal wieder gut sehen wie schnell es nach oben gehen kann mit den richtigen News. Darum habe ich mich auch entschieden hier keine schnellen gewinne mehr mitzunehmen und ich freue mich mit euch zusammen diesen weg gehen zu können. Und hoffe das wir uns weiter so gut austauschen und auch wenn es mal nicht so gut läuft einen guten umgang zu pflegen. Ich werde mich jetzt erst mal aufs Sofa werfen und mich von der Arbeitswoche erholen.

Cameron

http://www.irishexaminer.com/business/...-predicts-growth-248171.html

http://translate.google.de/...predicts-growth-248171.html&act=url

BoI changes its mind on economy, predicts growth

Friday, November 01, 2013

Bank of Ireland has changed its mind on the economy, saying it will show slight growth in 2013 before strengthening next year.

By Geoff Percival

Two months ago, the bank suggested the economy would remain flat in 2013, with 0% GDP growth likely.

However, in its latest quarterly economic outlook, published yesterday, Bank of Ireland said the slight recovery in the second quarter of this year (following contraction in each of the previous three quarters) leads it to expect GDP to rise by 0.4% this year, before rising by 1.9% in 2014.

In GNP terms — which excludes the contribution of foreign multinationals to the economy — Bank of Ireland expects to see 2.5% growth this year, followed by 1.5% next year.

The ESRI has forecast GNP growth of 2% for 2013 and 2.7% for 2014. The Central Bank recently lowered its GDP forecasts to 0.5% for this year.

Bank of Ireland’s change in sentiment comes on the back of a positive second-quarter turnaround in export performance and consumer spending; both of which — it expects — will show growth next year.

“We expect employment to rise further next year, which together with some modest pick up in earnings growth will boost personal disposable incomes and support consumer spending.”

Ireland’s export performance in 2014 should be driven by expected increases in the British, US, and eurozone economies, and result in 3.5% annual growth.

Consumer spending levels — although relatively flat this year — should rise by over 1%.

“The €2.5bn adjustment announced in Budget 2014 will have a dampening effect on economic activity,” Bank of Ireland said.

“However, we still expect domestic demand to increase by more than 1%, with a strengthening of investment — together with the increase in consumer spending — more than offsetting another fall in government spending.”

The bank expects inflation to remain subdued, the annual rate amounting to 0.7% this year and 1.1% next.

© Irish Examiner Ltd. All rights reserved

Optionen

| Boardmail an "Spaetschicht" |

Wertpapier: Bank of Ireland plc |

natürlich war der Hype von gestern Abend völlig übertrieben und die Anschlusskäufe fehlten ;

genau wie heute die Gewinnmitnahmen übertrieben waren ....

solange der Boden bei 0,26 cent hält sehe ich hier kein grosses Abwärtspotential warum auch :))

Optionen

| Boardmail an "Fritz1933" |

Wertpapier: Bank of Ireland plc |

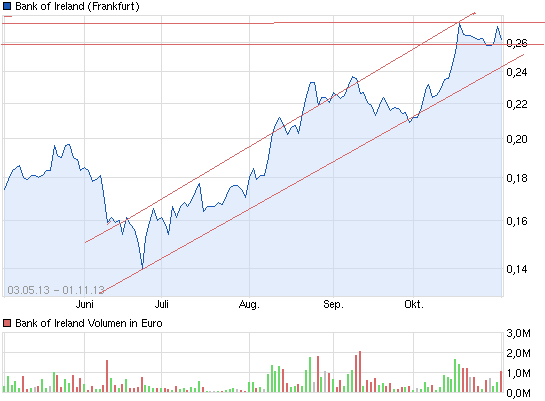

Angehängte Grafik:

2chart_free_bankofireland.png (verkleinert auf 93%)

2chart_free_bankofireland.png (verkleinert auf 93%)

Optionen

| Boardmail an "Fritz1933" |

Wertpapier: Bank of Ireland plc |

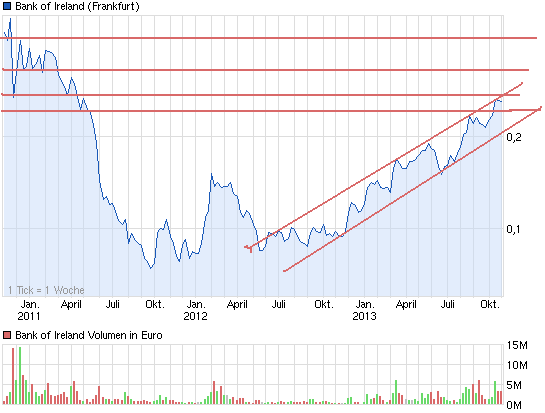

Angehängte Grafik:

3chart_3years_bankofireland.png (verkleinert auf 93%)

3chart_3years_bankofireland.png (verkleinert auf 93%)

Auch sollte ihnen mal jemand vor augen führen das ihre frustbedingten und anscheinend unter alkoholeinfluss geschriebenen posts niemanden tangieren(höchstens belustigen)!

Es zeugt auch nicht von hoher intelligenz immer und immer wieder andere user(deren invest-höhe sie nicht kennen da diese nicht mit stückzahlen prollen)als "kleinaktionäre" zu titulieren während man sich selbst phantasiestückzahlen zuspricht :-D

Wie soll ihnen jemand 20jahre börsenerfahrung abnehmen sowie ein alter von annährend 60!? wenn ihre posts denen eines gefrustetem 24jährigen mit .. sagen wir mal .. unterdurchschnittlichen iq entsprechen???

Hochachtungsvoll ;-)

bochum1848

Optionen

| Boardmail an "bochum1848" |

Wertpapier: Bank of Ireland plc |

hallo bochum 1848,

ich bin 120% Deiner Meinung.

Freue mich schon auf Montag und bin mal gespannt, wo wir da so liegen werden. Meine persönliche Erwartung liegt bei einer sehr leichten Steigerung. Der Chart begann morgens (ca.09:00 bis 10:00 Uhr) immer sehr hoch, gefolgt von einem anschließend fallenden Kurs bis fast zum Ende des Handelstages. Eine Erholung kam dann gegen 17:20-17:30 Uhr.

Gruss an alle boianer .