Jinkosolar - hat die niemand auf dem Radar?

Nur meine Meinung und keine Empfehlung.

Allen viel Glück hier.

BLUE

http://www.ariva.de/forum/...lennium-vor-dem-Durchbruch-421602#bottom

am 26.08.2010 meldet S2M den Rückkauf einer mittelbaren Beteiligung von 25 % an Ibersol von der Cross Capital AG. Konkret hat S2M 50 % der Anteile an der Soliber für 500.000 EUR erworben!

http://www.solarmillennium.de/deutsch/archiv/...10_08_26-ibersol.html

Am 03.11.2010 meldet S2M den Verkauf von 16 % an Ibersol an die Extremasol Kraftwerks GmbH. Wie oben nachgewiesen, belief sich der Veräußerungspreis auf 20,040 Mio. EUR!!

In diesem Zusammenhang drängen sich zwei Fragen auf:

1. Warum veräußerte die Cross Capital AG nicht die 16 % an Ibersol direkt an die Extremasol Kraftwerks GmbH?

1.1. Offensichtlich bevorzugte Cross Capital einen Kaufpreis in BAR in Höhe von 500.000 EUR einem Kaufpreis über 20 Mio. EUR (der jedoch bis auf weiteres nicht sehr werthaltig war).

2. Hatte S2M mit Cross Capital AG eine Rückkaufsoption über die 50 % Beteiligung an Soliber GmbH für 500.000 EUR vereinbart? In diesem Fall stellt sich die Frage, ob die Cross Capital AG überhaupt irgendwann einmal wirtschaftliches Eigentum an der Soliber GmbH erworben hat. Für den Fall, dass dies zu verneinen ist, ist der Konzernabschluss 2009/2010 fehlerhaft.

Wie man es wendet, die Widersprüche sind kaum auflösbar. Die Gläubiger haben m.E. ein Recht auf eine minutiöse Aufklärung.

Ich verstehe das nicht ... im Voraus vielen Dank für Deine Erläuterungen.

BLUE

Moderation

Zeitpunkt: 31.10.13 08:21

Aktion: Löschung des Beitrages

Kommentar: Regelverstoß - Userhetze bitte einstellen.

Zeitpunkt: 31.10.13 08:21

Aktion: Löschung des Beitrages

Kommentar: Regelverstoß - Userhetze bitte einstellen.

Weitermachen

Optionen

| Boardmail an "hollewutz" |

Wertpapier: Jinkosolar Holdings Com |

Moderation

Zeitpunkt: 30.10.13 12:36

Aktion: Löschung des Beitrages

Kommentar: Off-Topic - Bitte zum Threadthema zurückkehren und die Sticheleien einstellen.

Zeitpunkt: 30.10.13 12:36

Aktion: Löschung des Beitrages

Kommentar: Off-Topic - Bitte zum Threadthema zurückkehren und die Sticheleien einstellen.

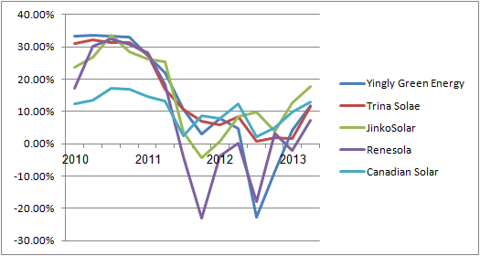

interessanter Artikel über die Technik :Polysilikon.Wafers,Module...Effektivität

was die einzelnen Firmen herstellen,Downstream und Upstream

und eine schöne Karte über

Solar Companies Groos Margin 2010-2013

http://static.cdn-seekingalpha.com/uploads/2013/...899534122_rId7.png

{kind=link}

...Recently, more and more module manufacturers have been entering the downstream side of the industry. China's recent policy guarantees a feed-in tariff (FiT) for utility scale projects for a period of 20 years, thus making them a sound investment....

..The polysilicon market is extremely oversupplied. According to SolarPVInvestor.com, the world has the capacity to produce about 550,000 metric tons of polysilicon, which translates into just over 100GW of module production per year. With polysilicon costs now above cash costs for many producers, I expect some Tier 2 and Tier 3 producers to exit the business in the coming years.

I see just a modest opportunity for polysilicon capacity to expand in the coming years, and I expect most of the CapEx to go toward equipment upgrades, which will ultimately enhance profitability for the companies that will be able to afford them.

With the global demand for solar panels on the rise, the PV industry recently returned to profitability and a few companies have even shown double-digit gross margins. To determine which company is best positioned to capture value going forward, let's look at the industry's production capacity.

Demand has been increasing in recent quarters. After a rough 2012, demand is now expected to reach ~40GW this year, up from 32GW last year.

Most demand today comes from utility scale projects. Different countries around the world have various renewable energy policies in place. In the past, companies looked for subsidized markets, as the cost of generating solar power was higher than the local selling price of electricity. Today, in most parts of the world, solar power has a lower LCOE than local electricity prices. The situation in the U.S. is such that in most states, a solar project can be implemented and generate power in a lower cost than the retail price of electricity......

In China, the leading country in terms of global demand for solar panels, a new policy was recently introduced. Under this policy, a FiT of 0.90-1 RMB (about 14¢-17¢) is offered to utility scale project owners. JinkoSolar and Yingli Green Energy have already taken advantage of this lucrative offer. Yingli recently demonstrated the IRRs it can achieve in China......

Manufacturers can choose to sell projects to investors, but in the long run, it is more profitable for them to keep projects and sell the electricity they generate. ...

Die Kapazität der einzelnen Firmen findet sich auch in einer Darstellung

http://www.ariva.de/forum/...dem-Radar-418576?new_pnr=16732716#bottom

Moderation

Zeitpunkt: 31.10.13 08:21

Aktionen: Löschung des Beitrages, Nutzer-Sperre für 2 Stunden

Kommentar: Regelverstoß - Userhetze bitte einstellen!

Zeitpunkt: 31.10.13 08:21

Aktionen: Löschung des Beitrages, Nutzer-Sperre für 2 Stunden

Kommentar: Regelverstoß - Userhetze bitte einstellen!

Mehr schreib ich jetzt aber nicht zu den zwei, denn interessieren tut es eh keinen und die zwei sind für mich uninteressanter als wenn in China ein Sack Reis umfallen würde.

Damit deise Post wenigstens einen kleinen informativen Charakter hat: Sunpower bringt heute Abend ihre Q3-Zahlen und First Solar morgen. Diese Q3-Ergebnisse der beiden US Solarunternehmen sind zwar für Jinko nicht von allzu hoher Relevanz, aber interessant sind sie allemal.

Optionen

| Boardmail an "ulm000" |

Wertpapier: Jinkosolar Holdings Com |

http://www.forbes.com/sites/narrativescience/2013/...partner=yahootix

.... This is a vitally important week for publicly traded solar stocks, and if the company doesn't live up to expectations when it reports quarterly earnings on Halloween, we'll probably see First Solar take another steep stumble in just a few days.

http://www.fool.com/investing/general/2013/10/28/...n-the-sp-500.aspx

Desertsun scheint sich auch mit dem Pinksheet BYDDF gut auszukennen,er hat eine unglückliche Liebe zu hochverschuldeten Firmen kurz vor dem Bankrott und lamentiert dann rum

Ich hatte Dir vor Tagen ja schon eine BM geschickt: tendenziell wohlwollend, konstrukiv, wie ich fand - schlicht, weil in Deinen Zeilen soviel Verzweiflung, Destruktion, (Selbst-)Hass steckt. Scheint nix genutzt zu haben....

Deshalb jetzt noch einmal öffentlich und völlig kostenlos: Ich kenne Dich zwar nicht, aber mache Deine Frieden, mit andern und vor allem mit Dir selbst, komme mal runter von deinem Psychotripp, sonst wird das an der Börse und, sorry, auch darüber hinaus nix mehr...

Optionen

| Boardmail an "Eskimoo" |

Wertpapier: Jinkosolar Holdings Com |