silverado goldmines (867737)

Optionen

| Boardmail an "18prozent" |

Wertpapier: Silverado Gold Mines |

By Aaron L. Task

Editor at Large

6/12/2007 12:56 PM EDT

Click here for more stories by Aaron L. Task

While the mainstream press focuses on Monday's symbolic "no confidence" vote over Attorney General Alberto Gonzales, the Senate also took up the energy bill, legislation with far-reaching implications for investors and at least one presidential candidate.

Fuel-efficiency standards for automakers, and renewable energy requirements for utilities will dominate the headlines, but amendments promoting coal-based fuels fall squarely into the "politics makes strange bedfellows" department.

It turns out Democratic presidential aspirant and Illinois Sen. Barack Obama has more in common with the U.S. Air Force than the Natural Resources Defense Council or Moveon.org when it comes to solving America's dependence on foreign oil.

Both Obama and the Air Force have determined the path to energy independence runs through the coal mines of Appalachia, Wyoming and, yes, Illinois. This unlikely pairing has both political and investing implications for those gaming the possibility of an Obama presidency.

Coal's political appeal is clear: There are more than 250 billion tons of recoverable coal reserves in the U.S., the equivalent of about 800 billion barrels of oil, or more than three times Saudi Arabia's proven oil reserves, according to the National Mining Association.

Thus, while the popular press, celebrities and a certain former vice president focus on "greenhouse gases," the energy bill is likely to contemplate recent legislative proposals such as taxpayer-funded loan guarantees to build coal-to-liquid plants.

Spearheading current legislation in the House are Rick Boucher (D., Va.) and Geoff Davis (R., Ky.), while Senate sponsorship is coming from Republican Jim Bunning of Kentucky, who co-sponsored the Coal-to-Liquid Fuel Promotion Act of 2007 with Obama in January.

Illinois ranks as the nation's seventh-leading coal producer, according to the Department of Energy. Nearly 32 million tons of Illinois coal were mined in 2005, generating nearly $1 billion in gross revenue, according to the Illinois Department of Commerce.

Such statistics help explain Obama's support for coal-based initiatives. But amid a January backlash from environmentally conscious Democratic primary voters, Obama largely ceded leadership on the issue to Bunning.

In May, Bunning and the late Craig Thomas (R., Wyo.) proposed to diminish the role of ethanol in the energy bill and mandate the use of 21 billion gallons of coal-based fuels by 2022. The amendment was defeated in the Senate Energy and Natural Resources Committee by a 12-11 vote on party lines. (Obama is not a committee member.)

Coal Gets Greens Red in the Face

Environmental groups oppose coal-to-liquids because nearly two times the carbon dioxide is emitted in the production of coal-to-liquid, or CTL, vs. traditional petroleum fuels.

"In a nutshell, CTL is worse than conventional fuels," says Elizabeth Martin Perera, climate policy specialist at the Natural Resources Defense Council, a not-for-profit organization. "CTL has higher life-cycle CO2 emissions than conventional fuels, even with carbon capture and storage."

http://www.thestreet.com/_tscrss/funds/investing/10362048.html

steigendes Volumen fallender Kurs, da müßte doch mal langsam die Trendwende eingeläutet werden!

Optionen

| Boardmail an "tornadotoni" |

Wertpapier: Silverado Gold Mines |

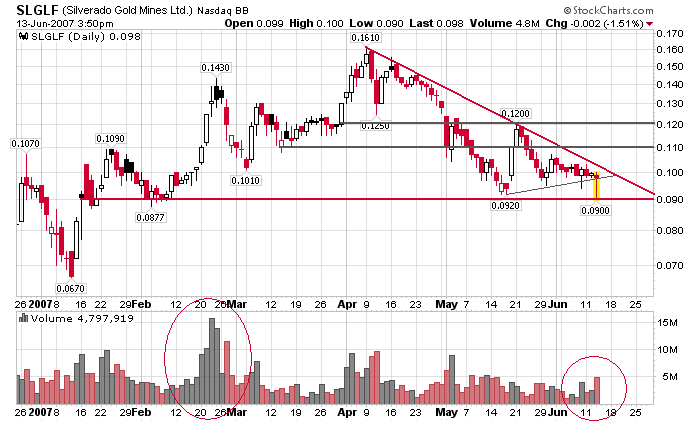

Angehängte Grafik:

chart.png (verkleinert auf 72%)

chart.png (verkleinert auf 72%)

Dafür mal komplett ohne Linien ;-)

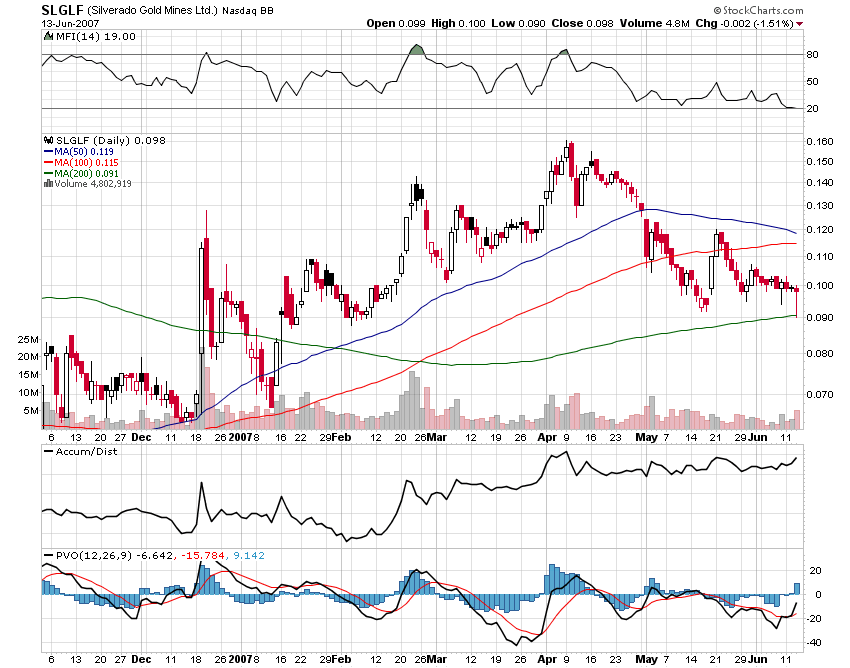

Erklärung:

MFI:

ist eine umsatzgewichtete Variante des RSI

Der Money Flow Index gehört zu den Trendfolgern und bezieht neben den Kursen auch die Umsätze in die Berechnung ein. Er stellt eine Art Umsatz-Momentum dar.

Kaugsignal: Schlusskurs in der Nähe des Tageshochs

Verkaufssingal:Schlusskurs in der Nähe des Tagestiefs

Accum/dist:

Komkbination aus Volumen- und Preisdaten

Kaufsignal liegt vor, wenn der Indi keine niedrigere Tiefen bildet, während der zu Grunde liegende Aktienkurs neue Tiefs generiert.

In jedem Fall deutet eine Abweichung eine Umlenkung in der dominierenden Tendenz an.

(bzw. kann nahe sein an)

PVO:

Ist der Abstand zwischen zwei langfristigen volumen bezogenen MA's, in Prozent angegeben.

Wenn die Aktieneue Höhen generiert, sollte der Indi folgen. Tut re dies nicht ist es ein Warnsignal. Andererseits tritt ein Kaufsignal auf, wenn der Indi keine neuen Tiefen bildet, während die Aktie dies tut. In jedem Fall deutet eine Abweichung eine Umlenkung in der dominierenden Tendenz an.

(bzw. kann nahe sein an)

Angehängte Grafik:

sc.png (verkleinert auf 60%)

sc.png (verkleinert auf 60%)

Die setze ich bei Silverado überigens immer auf.

Sway hat mir dieses Model mal empfohlen ;-)

Für alle ohne Spezialbrille verrate ich nun was ich sehe :

Das Tal ist durchschritten. Die Hügel liegen hinter uns. Vor uns stehen bald nur noch

Gebirgsformationen ungeahnten Ausmaßes.

So Gott will.

http://smallcapmedia.com/articles/...ls-exploration-june-12-2007.html

NEW Silverado Gold Mines Ramps Up Its Placer Gold Production and Now Believes It has the Prolific ‘Mother Lode’ Source Within its Reach

By Marc Davis

June, 2007

Corporate Overview

Silverado Gold Mines Inc. (NASD OTCBB:SLGLF) (Frankfurt: SLGL) (Berlin: SLGL) is a diversified natural resources company that is riding the crest of two major trends – one involving a sustained bull market for gold prices and the other being the imperative to develop innovative new forms of inexpensive ‘green energy.’

For more on Silverado Green Fuel Inc., a wholly-owned subsidiary, please refer to Part II of this investment assessment.

All told, Silverado (www.silverado.com) has spent about a quarter of a century developing prospectively world-class gold projects in mineral-rich Alaska – home to some of North America’s most prolific gold mines and developmental stage gold deposits.

Moreover, Silverado’s progress has thus far been quite lucrative. In fact, while hunting for major ‘lode’ deposits, the Company has carved a profitable business niche for itself in the placer gold mining business. And all of this placer gold is known to have originated from nearby buried concentrations of gold that represent the ultimate prize or ‘mother lode.’ Specifically, the placer gold has leached out of rich proximal gold vein/shear structures into river drainage systems, where over the millennia it has become part of ancient gravel beds.

While Silverado continues to use sophisticated geo-scientific sleuthing technology at its Nolan Property to zero-in on the exact location of the buried lode treasure trove, the Company is also building considerable intrinsic value into its share price by way of its steady stream of gold revenues.

This gives Silverado a pronounced competitive advantage over legions of other gold exploration juniors that have no gold production to sustain them. Instead, they have nothing but grandiose dreams of winning the mineral exploration jackpot to justify their much-hyped share prices. By comparison, Silverado is still very modestly priced.

To date, the Company’s tangible gold assets have generated over U.S. $20 million in sales since the 1980’s – much of it in gold and silver bars and the rest in sizeable gold nuggets which are highly sought after for Alaskan jewelry.

In essence, this placer gold mining business serves as a financial backstop for a ‘best of both worlds’ business mode. One that provides meaningful and consistent cash-flow, as well as a commitment to finding the lode source of all of its placer gold.

Notably, more than half of all of Silverado’s gold revenues were generated in 2006, alone. This resulted from the recommencement of underground mining at the Company’s wholly-owned Nolan Mine. This suggests that Silverado may be starting to tap into remnants of very rich lode vein systems along a prolifically mineralized trend or horizon. This represents the culmination of 16 years of systematic exploration of the expansive Nolan Property for the source of the placer gold.

All told, an estimated 354,686 troy ounces of gold resources have so far been delineated by mining and drilling on Silverado’s Alaskan properties, according to independent geological reports.

Canadian investors should note that this mineral resource estimate is not National Instrument 43-101 compliant as Silverado does not operate its gold projects in Canada. (In other words, this resource figure does not satisfy guidelines that constitute a Canadian federal government recognized standard for a “mineral reserve.”)

The Emerging Nolan Gold Deposit/Mine: An Overview

Some of Silverado’s gold resources have to date been outlined at the developmental stage Nolan Gold Mine. Located 280 road miles north of Fairbanks in the state’s Arctic Circle region, it is the site of an extremely cost-efficient and profitable surface mining operation for gold-bearing gravel. In the winter, underground mining of frozen gravels also takes place, allowing for year-round revenue generation.

In the summer months when the gravel has thawed, snow melt water is available for gold recovery by sluicing. Environmentally conscious investors will be happy to learn that the sluicing process uses only gravity and water within a closed circuit, ensuring that there is zero discharge to the environment. Also, lands disturbed by the Company’s mining activities are fully reclaimed.

Most of the gold found at the Nolan Mine is in nugget form. This offers a distinct advantage over conventional mining methods that typically involve crushing and grinding large volumes of rock to extract gold particles. Instead, Silverado’s nuggets can be easily and inexpensively extracted from the gravels and sold for a hefty premium to their melt-down value (averaging about 33% above bullion’s spot price).

For instance, one nugget recovered at Nolan weighed 41.35 ounces and sold for U.S. $50,000 – a 212% premium above its melt-down value. Another weighing 13.78 troy ounces was taken from the floor of the Nolan Mine’s Mary’s East Tunnel after a controlled blast as recently as February of this year.

Tapping into a Rich Vein of Opportunity: 2006 Nolan Exploration Highlights

Silverado believes that the increasing frequency of sizeable gold nuggets being found at the Nolan Property suggests that the Company is zeroing-in on their lode source. This is where gold in water flows through fissures or the spaces between cracks in rocks, where it precipitates out. In turn, this forms ‘ore-zones’, or rich quartz gold veins, such as the ones that Silverado has encountered during last season’s drilling and trenching programs.

During the fall period of Silverado’s 2006 exploration program, Silverado also carried out a total of 920 feet of backhoe trenching to investigate gold bearing antimony-quartz vein systems. Ones that are part of the Solomon Shear, a five mile long gold bearing shear zone (which is a geologically favourable structure for the emplacement of significant gold deposits).

Such developments constitute a major exploration breakthrough for Silverado. This allowed the Company to announce that it was beginning to outline the parameters of what it describes as a “significant gold/antimony deposit.” A discovery that Silverado CEO Garry Anselmo says may be a “potentially huge source of gold.” One that will be aggressively explored in 2007.

That said, the discovery of high-grade gold zones is now a function of the methodical development of the sizeable Solomon Shear Trend, which may prove to host many rich gold zones, each with multi-million ounce potential.

An airborne geophysical survey published by the State of Alaska is also being used in conjunction with on-going ground geological, geophysical, and geochemical surveys to pin-point the exact location of such enriched gold zones

Meanwhile, of the three mineralized zones identified to date by trenching, the ‘main zone’ was revealed to host 16 gold veins across a zone of alteration 192 feet wide. A total of 71 combined chip and channel rock samples were collected during the trenching program and submitted to ALS Chemex in Fairbanks for analysis.

Out of these 71 samples, 32 show values higher than 0.01 ounces of gold per ton (opt) and ranged from 0.01 opt to 0.83 opt. These results offer clear confirmation that high-grade lode gold mineralized quartz veins exist in the Solomon Shear Zone, according to Silverado’s geological team.

Drilling at Nolan Reveals a High-Grade Antimony Discovery

Another notable coup for Silverado in 2006 was the discovery at the Nolan Deposit of rich antimony values, running from 1% to 46% in rock samples. To put this in dollar terms, rock containing 46% antimony would be worth about U.S. $2,300 per ton (at the current antimony price of $2.56/lb). By comparison, the same ton of rock would have to contain roughly 3.5 ounces of gold per ton (at $656/ounce) to be of the same monetary value.

Preliminary metallurgical tests on Nolan’s antimony samples showed combined lead and arsenic present in amounts less than 0.1%, which constitutes some of the purest antimony in existence, according to Silverado. This is very important since antimony contaminated with over 0.5% combined lead and arsenic has to be shipped overseas to be processed.

Antimony Prices Are Poised to Spike Higher

Antimony is a silvery-white metal with a very low melting point and is used in North America primarily in chemicals. It is most commonly used to impregnate plastics, textiles, rubber and other materials as a flame retardant. Antimony is also mixed with other metals to increase their hardness and strength, such as batteries and the lead in bullets, and it is also considered a military strategic metal. It is also used to seal the fire sprinklers which when heated melt and allow the water to flow.

As an aside, China produces 82% of the world’s antimony, Russia 8%, South Africa 3%, Tajikistan 2% and Bolivia 2% (for a total of 97%). In November 2006, China indicated that it would cut its export quotas of antimony and tin by 30%, which will likely create a supply squeeze.

In turn, antimony prices are almost certain to surge higher, which is nothing but good news for Silverado. This is particularly the case since North America accounts for only a fraction of global production, while it accounts for most of the world’s industrial usage.

Other Key Developments

In 2005, the Company began underground mining on the Swede Channel portion of the Nolan Mine, involving the implementation of extensive infrastructure and mining equipment and other support facilities. This gold-rich zone yielded 939 ounces of gold last year, 785 of that being high premium nugget gold.

However, that figure only represents a portion of the gold that has already been outlined in the Swede Channel. In fact, only about 30% of the Swede ore zone was removed in 2005/06. The balance of the ore, along with a newly discovered extension to the Swede Channel, was mined out in the winter of 2006/07. The resultant 18,000 cubic yards now await gold extraction, which will begin later this month.

Widespread Regional Gold Potential Including Silverado’s Hammond Property

The Company has also optioned property that covers the adjoining Hammond River placer deposits. The Hammond Property adjoins the Nolan project to the northeast. It contains the Slisco Bench, a prime placer prospect and one of Silverado’s future exploration targets.

Silverado therefore plans to conduct drilling to delineate additional gold resources, while also gaining geo-technical and engineering data for potential mining of this ancient riverbed.

The Hammond River is historically and currently a rich gold producer in the district. Exploration to date, including 103 drill holes, reveals that the Slisco Bench is an attractive underground prospect which may prove to be a significant gold producer in the future.

Notably, the Company drilled 33 holes on this bench in 2006 with 15 of them hitting significant gold values. These values ranged from 0.01 to 0.5 ounces of gold per bank cubic yard of gravel.

Other Key Assets

In addition to the Nolan Gold Deposit, the Company also owns the Ester Dome Gold Project, as well as the Eagle Creek Project, both of which are located close to Fairbanks, Alaska. Significantly, they are also part of the same gold belt where Kinross is operating its huge Fort Knox Gold Mine. Likewise, Kinross’ True North Gold Deposit is also in close proximity to both of these geologically very prospective projects.

Historically, the Eagle Creek Property was Alaska’s second largest antimony producer. In the late 1980’s, Silverado built a 100-ton-per-day gravity plant and processed the old mine dumps, successfully selling all the antimony produced. Although Silverado originally studied this property for its antimony potential, the constant discovery of gold soon changed the property status from antimony to gold/antimony.

In addition to the high-grade gold bearing quartz veins found on Silverado’s large Eagle Creek property, the Company also made a significant new gold discovery at the project area in 2006. This new discovery area shows gold dissemination throughout intrusive rocks and will be better investigated at a future date.

At the Ester Dome Property, Silverado has sporadically worked the area since 1978 to present. This includes the development of lode gold deposits on the Grant Mine portion of the project area. All told, this has in the past yielded some U.S. $10 million in high-grade gold bullion bars.

An extensive exploration program in the mid 1990’s at the St. Paul Shear Zone on Ester Dome resulted in the discovery of a potentially large lode gold ore body. Since then, only a small but representative part of the property has been drilled to very limited depths on gold mineralized zones which are “open” (continuous) to a vertical extent at depth and along a lateral plane (strike length).

This is also the case with the O’Dea and Ethyl-Elms mineralized zones on this highly attractive Ester Dome Property where a recorded four million ounces of placer gold have been taken from around the base of this small mountain.

The Company therefore believes that it has only just ‘scratched the surface’ of what remains a potentially very rich gold property with plenty of ‘blue sky’ potential. However, Silverado has strategically decided to focus the bulk of its near-term exploration activities at the Nolan Property.

Moreover, an outdated 300-ton-per-day gold processing facility is the legacy of a highly productive lode mining era at the Easter Dome Property. This mill complex is worth at least U.S. $6 million in 2007 dollars and is being relocated to Mississippi to provide valuable processing infrastructure for the Company’s fledgling Green Fuel business.

Investment Summary

Shareholders of Silverado Gold Mines are in an enviable position. They have considerable exposure to a rising tide market for gold prices, as well as for antimony. Not only does this come in the form of the ‘blue sky’ potential for finding a prolifically rich ‘mother lode’ style gold deposit at the Nolan Property; but it also can be measured in more tangible terms by way of the Company’s small-scale but very lucrative placer gold mining operation.

Then there’s an additional dimension to the Company by way of Silverado’s radically non-linear diversification into the 21st century alternative energy business. This involves its wholly owned subsidiary, Silverado Green Fuel Inc.

The Company’s ‘green’ alternative fuel source heralds a major breakthrough in inexpensively solving North America’s addiction to dwindling foreign oil reserves. And it could substantially help mitigate carbon dioxide emissions, nitrous oxides, sulfur dioxides and particulate matter throughout the industrialized world, as well. With a much sought-after business model for the wide-scale commercialization of this clean fuel initiative, Silverado certainly has a tiger by the tale.

SmallCapMedia therefore believes that a convergence of powerful value drivers is now setting the stage for a very bright and dynamic future for Silverado. One that promises to reward patient investors with considerable ‘home run’ potential.

Hence, SmallCapMedia believes that the share price of this enterprising, up-and-coming Company will continue to establish a sustained upwards trend during the balance of 2007. And the advent of plenty of ‘blue sky’ potential at its gold projects and its green energy venture should provide a powerful springboard for Silverado’s share price in 2008 – a time when SmallCapMedia expects to see the Company’s stock trading at many multiples of its current price.

Notably, more than half of all of Silverado’s gold revenues were generated in 2006, alone. This resulted from the recommencement of underground mining at the Company’s wholly-owned Nolan Mine. This suggests that Silverado may be starting to tap into remnants of very rich lode vein systems along a prolifically mineralized trend or horizon. This represents the culmination of 16 years of systematic exploration of the expansive Nolan Property for the source of the placer gold.

Und gehen einmal in USA wegen Strommangel die Lichter aus oder den Jets der Sprit ,

dann wird hier erst so richtg durchgestartet werden:-)

By Marc Davis

June, 2007

Corporate Overview

As an emerging gold mining company ( NASD OTCBB:SLGLF ) (Frankfurt: SLGL) (Berlin: SLGL) , Silverado Gold Mines Ltd.’s bottom line is as sensitive to surging oil prices as any other energy-dependent producer of mineral resources. Likewise for the rest of the world’s industrial infrastructure, which is also beholden to global oil oligopolies, better known as cartels.

However, whereas this energy supply squeeze spells trouble for most, Silverado (http://www.greenfuel.com/) amazingly sees nothing but a big ‘blue sky’ of unprecedented opportunities. That’s because this enterprising company has taken the extraordinary landmark step of remedying the problem at its very source.

That is to say, Silverado’s wholly-owned subsidiary, Silverado Green Fuel Inc., has pioneered the refinement of a cost-efficient, environmentally-friendly alternative to oil. We’re talking about the conversion of low-rank coal (of which the U.S. has an abundance) into liquid fuel, or environmentally-friendly fuel source.

This low-grade coal goes by the unwieldy term: low-rank coal-water fuel (LRCWF). This lignite coal has traditionally been of little use to most industrialized nations due to its high water content and therefore its inferior quality to other efficiently burning fossil fuels, including other types of coal. Even though over one-quarter of the world’s coal reserves are in the United States, half of those reserves are low-rank coal.

However, Silverado’s proprietary coal-to-liquid conversion technology has found an innovative multi-application use for this denigrated form of coal. Silverado’s cutting edge solution is simply referred to as a Green Fuel. This is a very fitting name as this fuel source is non-toxic, non-hazardous, non-flammable during creation and transportation and it burns very clean.

All told, it can be used for electricity generation, industrial heat and in the production of various fuels, ranging from a low-cost gasoline alternative to ultra-clean diesel, jet fuel and synthetic natural gas. It also has a multitude of other industrial applications, even including other environmental technologies such as hydrogen for turbines and fuel cells.

Too good to be true? Well, not according to the U.S. federal government, as well as the coal-rich state of Mississippi. The latter is seizing the initiative to become the first U.S. state government to take a major roll in financing and further developing this new ‘green’ energy form. Meanwhile, the U.S. federal government is also beginning to move in the same direction, as we will discuss later on in this article.

The desire at the highest levels of the U.S. government to embrace this new fuel form is being spurred on by a realization that the U.S. must significantly reduce its dependence on foreign oil. It must therefore move towards energy self sufficiency. The economic benefits to the U.S. cannot be overstated either since it boasts the world’s largest coal reserves and has enough coal to meet its energy needs for at least the next two centuries.

This new paradigm shift is not lost on Silverado’s Company CEO, Garry Anselmo, who recently met with SmallCapMedia. During the interview, he obviously had plenty to smile about, though he is far from smug. He merely exudes the demure self-assurance of a man who knows that his Company’s contribution to society will be far reaching – and will meet the approval not just of his shareholders but also of his grand-children, too.

"If a ship breaks apart, you have water and a substrate that is conducive to plant growth. If a pipeline ruptures, you have water and particles that can be scooped up and reconstituted,” he states in a matter-of-fact manner.

“It (Green Fuel) is non-toxic, non-hazardous, nothing dies. No birds are hurt in spills," he adds. “But we’re not just talking about helping the environment here. We’re also talking about the launching of a multi-billion dollar business.”

In addition, licensing this technology to developing nations will help to diminish the amount of greenhouse gases emitted to the atmosphere worldwide. However, the biggest market for this fuel form is in Silverado’s back yard. In fact, over half of the electrical power created in the United States today is generated from the direct burning of coal.

Work on a Government Co-Funded US $26 million Demonstration (and Future Production) Facility in Mississippi Gets Underway .............

http://www.smallcapmedia.com/articles/...tech-focus-june-10-2007.html

Es tut sich also was.

bei

unter zehn cent ist wahrlich zu billig. der spread bringt einen ja schon um!!

nicht zu empfehlen.

vg, paro

Optionen

| Boardmail an "Parocorp" |

Wertpapier: Silverado Gold Mines |

Optionen

| Boardmail an "SWay" |

Wertpapier: Silverado Gold Mines |

Ohne news bleiben die 0,1 $ leider unüberbrückbar.

so long

Keine Sorge, ES WIRD RAUF GEHEN !

aber Burns hat nichts mehr zu gewinnen nur noch ALLES zu verlieren und genauso

kämpft er auch mit dem Broker seines Vertrauens...

Das schöne am "normal" investiert sein ist, man kann max. 100% Verlust machen und das schafft keiner der hier investierten das ist schon mal klar aber als Shortie der immer dachte "naked shorts never ever have to cover..." kann diese, wird diese Aktie das Ende eines jeden Luxus bedeuten. Dann kommt noch die Scheidung dazu, ach wird das schön...

ich stelle mir gerne vor das Burns mit ca. 600-700. Mio. Aktien Short ist, mit sogenanten phantom shares... Würde das ein Fest wenn er versuchen müsste die zurückzubekommen. *lach*

Alles angeschnallt ?

Optionen

| Boardmail an "SWay" |

Wertpapier: Silverado Gold Mines |

http://www.sec.gov/news/press/2007/2007-114.htm

SEC Votes on Regulation SHO Amendments and Proposals; Also Votes to Eliminate "Tick" Test

FOR IMMEDIATE RELEASE

2007-114

Washington, D.C., June 13, 2007 - The Securities and Exchange Commission today voted to take additional steps to better safeguard investors and protect the integrity of the markets during short selling transactions by closing loopholes in Regulation SHO and further reducing persistent failures to deliver stock by the end of the standard three-day settlement period for trades.

Erik Sirri, Director of the SEC's Division of Market Regulation, said, "Today the Commission voted on steps to streamline and tighten short selling provisions so that markets and investors are better served by our rules."

1. Final Amendments to Rules 200 and 203 of Regulation SHO

The Securities and Exchange Commission voted to adopt final amendments to Rules 200 and 203 of Regulation SHO (17 CFR 242.200 and 242.203). The amendments will further reduce fails to deliver in certain equity securities by eliminating the grandfather provision. The amendments also modify the close-out requirement for fails to deliver resulting from sales of threshold securities pursuant to Rule 144 of the Securities Act of 1933 (Securities Act). In addition, the amendments update the market decline limitation referenced in Regulation SHO. The amendments will be effective 60 days from the date of publication of the amendments in the Federal Register.

Regulation SHO, which became fully effective in January 2005, provides a regulatory framework governing short sales of securities and, among other things, includes the following:

A definition of ownership for short sale purposes and a requirement to determine a short seller's net aggregate position.

A locate requirement, which requires that before accepting or effecting a short sale order, brokers and dealers must (i) borrow securities, (ii) make arrangements to borrow securities, or (iii) have a reasonable basis to believe that securities can be borrowed in order to make timely delivery.

Additional delivery or close-out requirements on designated "threshold securities." A threshold security means an equity security registered or required to file reports with the Commission for which there is an aggregate fail to deliver position for five consecutive settlement days at a registered clearing agency of 10,000 shares or more and that is equal to at least 0.5% of the issue's total shares outstanding. Where a clearing agency participant has a fail to deliver position in threshold securities that persists for 13 consecutive settlement days, the participant must take action to close out the position. Until the position is closed out, the participant, and any broker-dealer for which it clears transactions, including market makers, may not effect further short sales in the particular threshold security without borrowing or entering into a bona fide arrangement to borrow the security.

A grandfather provision that provides that the requirement to close-out fail to deliver positions in threshold securities that remain for 13 consecutive settlement days does not apply to positions that were established prior to the security becoming a threshold security or prior to the effective date of Regulation SHO. The grandfather provision was adopted because the Commission was concerned about creating volatility where there were large pre-existing fail to deliver positions.

The amendments voted on today will:

Eliminate the grandfather provision in Rule 203(b)(3)(i) so that all fail to deliver positions in threshold securities will have to be closed out within 13 consecutive settlement days, regardless of whether they occurred before the security became a threshold security.

Permit previously-excepted grandfather positions that are threshold securities on the effective date of the amendment to be closed out within 35 settlement days of the effective date of the amendment.

Amend Rule 203 of Regulation SHO to extend the close out requirement from 13 to 35 consecutive settlement days for fails to deliver resulting from sales of threshold securities pursuant to Rule 144 of the Securities Act.

Amend Rule 200(e)(3) to (i) reference the NYSE Composite Index (NYA) instead of the Dow Jones Industrial Average (DJIA); (ii) add language to clarify that the two-percent limitation is to be calculated in accordance with NYSE Rule 80A; and (iii) provide that the market decline limitation will remain in effect for the remainder of the trading day.

2. Proposed and Re-proposed Amendments to Regulation SHO

The Commission voted to propose amendments to Rule 200 and re-propose amendments to Rule 203 of Regulation SHO (17 CFR 242.200 and 242.203). The proposed amendments would modify the long sale marking requirements of Regulation SHO to require that broker-dealers marking a sale as "long" document the present location of the securities being sold. The re-proposed amendments are intended to further reduce fails to deliver in certain equity securities by eliminating the options market maker exception to the close-out requirement of Regulation SHO. In addition, the Commission voted to solicit comment regarding two narrowly-tailored alternatives to elimination of the options market maker exception.

The comment period for the proposals will end 30 days from the date of publication of the proposed rules in the Federal Register.

The options market maker exception provides that any fail to deliver position in a threshold security resulting from short sales effected by a registered options market maker to establish or maintain a hedge on options positions that were created before the underlying security became a threshold security do not have to be closed out. Today's proposed amendments would eliminate this exception to the close-out requirement of Regulation SHO. In addition, the proposed amendments to eliminate the options market maker exception would include a one-time 35 consecutive settlement day phase-in period for previously-excepted fail to deliver positions.

3. Amendments to Rule 10a-1 and Regulation SHO

The Commission voted to adopt amendments to Rule 10a-1 (17 CFR 240.10a-1) and Regulation SHO (17 CFR 242.200 et seq.) that will remove Rule 10a-1 as well as any short sale price test of any self-regulatory organization (SRO). In addition, the amendments will prohibit any SRO from having a price test. The amendments will also include a technical amendment to Rule 200(g) of Regulation SHO that will remove the "short exempt" marking requirement of that rule. The amendments will be effective immediately upon publication of the release in the Federal Register.

The Commission adopted Rule 10a-1 in 1938 after several years of considering the effects of short selling in a declining market. Rule 10a-1 provides that, subject to certain exceptions, a security may be sold short (A) at a price above the price at which the immediately preceding sale was effected (plus tick), or (B) at the last sale price if it is higher that the last different price (zero-plus tick). Short sales are not permitted on minus ticks or zero-minus ticks, subject to narrow exceptions. The operation of these provisions is commonly described as the "tick test." The tick test applies only to listed securities, other than Nasdaq-listed securities, traded on an exchange, or otherwise.

In addition to the tick test of Rule 10a-1, the NASD and Nasdaq have adopted their own short sale price tests based on the last bid rather than on the last reported sale for purposes of determining the execution prices of short sales. These bid tests apply only to Nasdaq Global Market securities that are traded on Nasdaq or the over-the-counter market and reported to a NASD facility.

On July 28, 2004, the Commission issued an order creating a one-year pilot temporarily suspending the tick test and any short sale price test of any exchange or national securities association for certain securities. The pilot was created so that the Commission could study the effectiveness of short sale price tests. The Commission's Office of Economic Analysis and academic researchers provided the Commission with analyses of the empirical data obtained from the pilot. In addition, the Commission held a roundtable to discuss the results of the pilot. The general consensus from these analyses and the roundtable was that the Commission should remove price test restrictions because they modestly reduce liquidity and do not appear necessary to prevent manipulation. In addition, the empirical evidence did not provide strong support for extending a price test to either small or thinly-traded securities not currently subject to a price test.

* * *

(ps. war effektiv eine Verwechslung mit ZN, passiert halt wenn man immer nur kurz auf den Screen schauen kann ,hab halt auch noch ein zweites Leben nebenbei )

L.G.